FEDERAL BUDGET 2026–27

In our ongoing pursuit to keep you informed and up to date on the current legislative climate, we have taken the time to put together a summary of the recent 2026–27 Federal Budget announced on Tuesday evening by Treasurer Jim Chalmers.

Below is a summary of issues that we believe are most relevant and valuable to our clients and not an exhaustive list of all Federal Budget measures. Many announcements remain proposals only and would need to be legislated to become law. If you would like to discuss what any of the measures below may mean for your personal situation, please contact our office.

At a glance – what stood out this year

The Budget was tax-centered, with the most significant proposals focused on:

- Capital Gains Tax (CGT) reform (replacement of the 50% discount with CPI indexation + a proposed minimum 30% tax on net capital gains)

- Negative gearing changes for residential property (redirecting concessions toward new housing supply)

- A proposed 30% minimum tax on discretionary trusts (from 1 July 2028)

- Targeted measures for workers (a proposed$250 Working Australians Tax Offset and an instant $1,000 deduction for work-related expenses)

- Superannuation was not the main event in this Budget, with limited new announcements made.

FAQs

- What are the key changes announced in this Federal Budget?

- Is the 50% Capital Gains Tax (CGT) discount being removed?

- How will Capital Gains Tax be calculated under the new proposed rules?

- Will the CGT changes apply to all investments or just property?

- What is changing with negative gearing for investment properties?

- Can I still claim property losses against my income?

- What are the proposed changes to discretionary (family) trusts?

- Has anything changed in superannuation as part of this Budget?

- What should I be doing now in response to these proposed changes?

Key dates

PERSONAL TAXATION

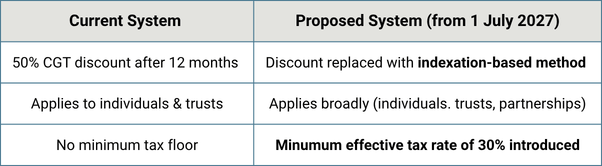

1) Capital Gains Tax (CGT) – major proposed reform (from 1 July 2027)

What is proposed

From 1 July 2027, the Government has proposed (subject to legislation) that:

- The 50% CGT discount for assets held more than 12 months would be replaced by cost base indexation (CPI)|

- A minimum 30% tax rate would apply to net capital gains

- These changes would apply broadly to CGT assets (including property and shares) held by individuals, trusts and partnerships (and would also apply to assets acquired prior to 20th September 1985 (Pre-CGT) assets, subject to transitional rules)

Important notes:

- Capital gains on pre-CGT assets arising before 1 July 2027 remain exempt under the proposed transitional rules. However, these assets are only CGT free from the date of purchase to the 1 July 2027 with the growth from this point forward subject to the new indexation rules.

- Income support payment recipients (including Age Pension recipients) would be exempt from the minimum 30% tax

- The Government has confirmed there are no proposed changes to the main residence exemption or the small business CGT concessions – however, the change in the first “step” of CGT calculation may affect outcomes in some situations (see example below).

Transitional rules – this is the part that matters most

If an asset is owned before and after 1 July 2027, the gain would be split:

- The portion of gains that accrue up to 30 June 2027 would generally retain the current tax treatment (including the 50% discount where applicable)

- Gains accruing from 1 July 2027 onward would be calculated under CPI indexation + minimum 30% tax rules

To do this, taxpayers will need to determine a CGT asset’s value at 1 July 2027 (via valuation, quoted prices, or an ATO tool/formula).

Client Callout – What this means for you

If you hold shares, managed funds, investment properties, or other CGT assets outside super:

- The after-tax outcome may change depending on the relationship between asset growth and inflation (CPI)

- There may be more emphasis on:

- valuation records (especially around 1 July 2027), and

- timing of future asset sales (particularly around retirement) due to the proposed 30% minimum tax

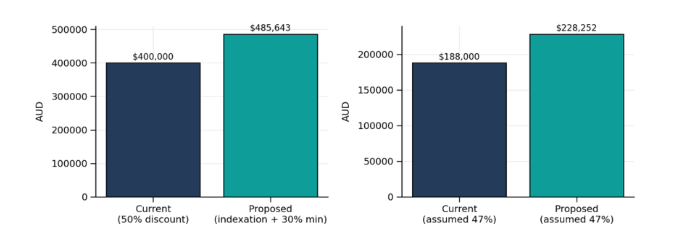

Example – How the proposed CGT changes could increase tax payable

The example above shows how the proposed CGT rules from 1 July 2027 may result in a higher taxable capital gain compared to the current 50% CGT discount rules.

An investor purchases an asset on 1 July 2022 for $800,000 and sells it on 1 July 2032 for $1.6 million.

At the start of the new rules on 1 July 2027, the asset is independently valued at $1,131,371.

Under the proposed transitional rules:

- The gain accrued before 1 July 2027 is $331,371.

- After applying the existing 50% CGT discount, the taxable gain is$165,685.

- The gain accrued after 1 July 2027 is $468,629.

- This portion receives cost base indexation, resulting in a taxable gain of $319,958.

This produces a total taxable capital gain of $485,643.

Under the current rules, applying a 50% CGT discount to the full $800,000 gain would have resulted in a taxable gain of only $400,000.

Assuming the investor is taxed at the top marginal tax rate of 47%:

- Tax under the proposed rules: approximately $228,252

- Tax under the current rules: approximately $188,000

This example highlights how the proposed changes could increase CGT liabilities for investors holding growth assets over the long term.

New build housing “choice” (CGT)

To maintain incentives for new housing supply, investors in new build residential properties would be able to choose either:

- the 50% CGT discount, or

- cost base indexation + the minimum tax

The definition of “new build” includes:

- dwellings constructed on vacant land, or

- where existing properties are demolished and replaced with a greater number of dwellings

Knock-down rebuilds or renovations that do not increase supply would not qualify.

Additionally, a new build cannot have been previously sold, unless first owned by the builder and not occupied for more than 12 months.

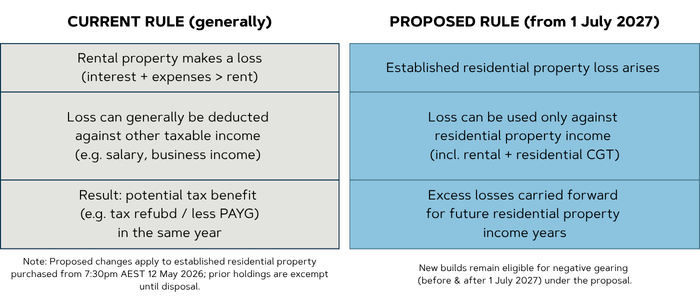

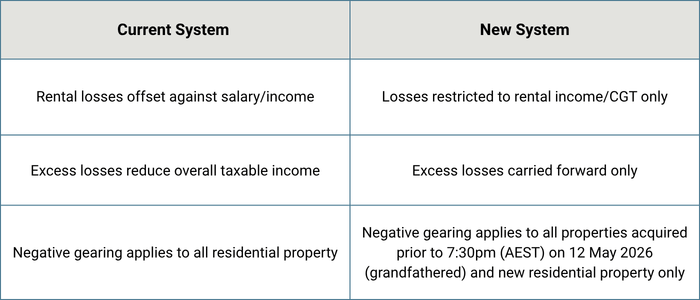

2) Reforming negative gearing (residential property)

The Government has proposed limiting negative gearing for residential property to new builds (from 1 July 2027, subject to legislation).

What is proposed

From 1 July 2027:

- Losses from established residential properties would only be deductible against residential property income, including rental income and residential capital gains

- Excess losses would be carried forward to offset residential property income (only) in future years

- The change would apply to individuals, partnerships, companies and most trusts

- Established residential properties acquired prior to 7:30pm (AEST) on 12 May 2026 (budget night) including contracts entered into but not yet settled would be exempt until disposed of

- Established properties purchased after 7:30pm (AEST) on 12 May 2026 would have the new rules applied from 1 July 2027

- Under the proposal New builds remain eligible for negative gearing (before and after 1 July 2027)

- Importantly, widely held trusts and superannuation funds including Self-Managed Superannuation Funds have been excluded from this measure.

Client Callout – What this means for you

If you already own an established investment property (held before the Budget cut-off):

- The proposal indicates you may retain negative gearing treatment until the property is sold, which creates an incentive to be deliberate about whether and when to dispose of grandfathered holdings.

If you’re considering buying an investment property in future:

- The proposal changes may increase the importance of reviewing:

- the differences between new and established properties; and

- alternative investment options such as shares/managed funds that are not impacted by these proposed property-specific negative gearing changes

- the differences between new and established properties; and

3) Medicare levy low – income thresholds

The Medicare levy low-income thresholds for singles, families, and seniors and pensioners are proposed to increase from 1 July 2025, including:

- Singles: $27,222 → $28,011

- Families: $45,907 → $47,238

- Single seniors/pensioners: $43,020 → $44,268

- Senior/pensioner families: $59,886 → $61,623

- Plus dependent child/student increment: $4,216 → $4,338

Client Callout – What this means for you

If your income is near these thresholds, you may remain exempt (or partially exempt) from the Medicare levy under the proposed increase.

4) Working Australians Tax Offset (WATO) – proposed

From 1 July 2027 (2027–28 income year), the Government has proposed a permanent annual $250 Working Australians Tax Offset applied against income derived from work (including wages/salary and sole trader business income), applied automatically after-tax return lodgement.

This measure could increase the effective tax-free threshold for work income by nearly $1,800 (subject to eligibility and legislative finalisation).

Client Callout- What this means for you

For many working Australians this is modest but positive and may slightly improve after-tax income from work once implemented.

5) $1,000 instant tax deduction – proposed

For the 2026–27 income year, the Government has proposed an instant tax deduction of up to $1,000 for work-related expenses where you claim less than $1,000 (i.e., without itemising). If work expenses exceed $1,000, you can continue to claim deductions in the usual way by providing evidence of these expenses.

Certain deductions (e.g. charitable donations, union/professional association fees and non-work related deductions) can still be claimed separately in addition to the instant deduction.

Client Callout – What this means for you

This measure is intended to simplify claiming for people with smaller work-related deductions, while preserving the ability to claim higher deductions where relevant.

TRUSTS & STRUCTURING

30% minimum tax on discretionary trusts (from 1 July 2028) – proposed

The Budget proposes introducing a 30% minimum tax on discretionary trusts from 1 July 2028, with the tax paid by the trustee on the taxable income of a trust.

Beneficiaries of discretionary trust income will be required to declare trust income, but beneficiaries (excluding corporate beneficiaries) will receive a non-refundable tax credit for the tax payable by the trustee.

Trustees that receive franked dividends will be required to use their franking credits to pay the 30% minimum tax.

Exclusions – The government have confirmed this minimum tax will not apply to the following types of trust:

- Complying superannuation funds

- Fixed and widely held trust (including fixed testamentary trusts)

|

- Special disability trusts

- Deceased estates, and

- Charitable trusts.

Discretionary testamentary trusts existing at announcement will also be excluded.

Rollover relief

The Government has indicated expanded rollover relief for three years from 1 July 2027 to support small businesses and others restructuring out of discretionary trusts into other entity types (subject to legislative detail).

Client Callout – What this means for you

If you operate a business or hold investments through a family/discretionary trust, this is a key area to watch. We expect many clients will need to review trust distribution strategies and structure once the final legislation is known.

If you require further information and advice regarding this change, we encourage you to contact your tax accountant.

Fringe Benefits Tax (FBT) – Electric Vehicles

The Government has announced changes to the Fringe Benefits Tax (FBT) treatment of electric vehicles.

From 1 April 2029, eligible electric vehicles will no longer be fully exempt from FBT. Instead, a reduced FBT rate (equivalent to a 25% discount) will apply for vehicles below the luxury car tax threshold.

Transitional arrangements mean that:

Vehicles entered into prior to this date may retain their existing concessional treatment

What this means

While electric vehicles will continue to receive concessional tax treatment, the benefit will be reduced over time compared to the current full exemption.

For clients considering:

- Novated leases, or

- Salary packaging arrangements

There may be an advantage in reviewing timing and structure before the proposed changes take effect.

If you require further information and advice regarding this change, we encourage you to contact your tax accountant.

SUPERANNUATION – QUIETER BUDGET NIGHT

CGT changes do not apply to super funds

Superannuation funds are not impacted by the proposed CGT changes and continue to be eligible for the 1/3 CGT discount where applicable.

Division 296- tax on large balances

Legislation has passed that from 1 July 2026 earnings attributable to the proportion of a superannuation balance above $3 million attract an additional 15% tax based on a pre-defined formula (with superannuation balances over $10 million attracting a further 10% tax on the proportion of earnings above $10 million).

Paid Parental Leave expansion (super contributions)

The government has proposed an expansion to Paid Parental Leave (to six months from 1 July 2026) means super contributions apply over a longer Paid Parental Leave period.

Client Callout – What this means for you

- Clients with higher superannuation balances should ensure plans are reviewed in light of the Division 296 tax changes taking effect from 1 July 2026.

BUSINESS TAXATION

Instant asset write-off – made permanent at $20,000

From 1 July 2026, the $20,000 instant asset write-off is proposed to be permanently extended for small businesses with turnover up to $10 million.

Loss carry – back reintroduction

For tax years commencing on or after 1 July 2026, it is proposed that eligible companies (with aggregated annual global turnover less than $1 billion) may be able to carry back tax losses and offset against tax paid up to two years earlier (subject to legislation and franking account constraints).

If you require further information and advice regarding the practical implementation of the above measures and whether they are relevant to you, we encourage you to contact your tax accountant.

OTHER MEASURES

Private Health Insurance rebate changes (older Australians)

From 1 April 2027, the Government proposes reducing the private health insurance rebate for Australians aged 65+ to align with the lower base rate for people under 65.

Foreign investment – established dwellings

The Government intends to extend the temporary ban on foreign purchases of established residential dwellings until 30 June 2029, with limited exceptions continuing.

OUR PRACTICAL TAKEAWAYS (how we expect clients will be affected)

If you are a property investor

- Existing established properties held before the cut-off may retain grandfathered negative gearing treatment until sale (under the proposal).

- The proposal changes may increase the importance of reviewing:

- the differences between new and established properties; and

- alternative investment options such as shares/managed funds that are not impacted by these proposed property-specific negative gearing changes

- the differences between new and established properties; and

If you hold investments outside super (shares/managed funds/property)

- Recordkeeping and valuation around 1 July 2027 becomes more important if the CGT proposal proceeds.

- The minimum 30% tax component may reduce the benefit of “selling in a low-income year” unless you qualify for an income support payment exemption.

If you use discretionary trust structures

- The proposed minimum tax may change outcomes for distribution planning once final details are known.

SOURCES

This update has been prepared using:

- firsttech-2026-27-federal-budget-briefing-paper

- netwealth-iq-federal-budget-2026-summary

- 2026-27-SMSF-Association-Budget-Summary

IMPORTANT NOTICE

The following relates to this document published by Stephan Independent Advisory.

GENERAL DISCLAIMER

The information contained in this update is general information only and is not intended to be a recommendation. We strongly recommend you seek advice from your financial planner as to whether this information is appropriate to your needs, financial situation and investment objectives.

Whilst every care has been taken in the preparation of this update, Stephan Independent Advisory, its directors, authors, consultants, editors and any persons involved in the preparation and distribution of this newsletter, expressly disclaim all and any form of liability to any person in respect of this update and any consequences.