This case study shares with you the type of process we go through with our clients here at Stephan Independant Advisory. If you relate to any part of this case study, get in touch with us today so we can help you manage your wealth for the next generation.

A Cleaning Enterprise

Sam and Kylie Hatfield operated a successful manufacturing business that provided cleaning products to commercial cleaners. The business was built on many years of blood, sweat, and tears, and was valued at more than $10 million.

Shortly after his 60th birthday, Sam realised that it was time to think seriously about retirement – but it’s a difficult prospect when you’ve been self-employed all your working life, and a large portion of your retirement savings are tied up in the business.

Sam and Kylie have three adult children and seven grandchildren. They live for their family and wanted to ensure that while enjoying a comfortable and fulfilling retirement, their family would also be provided for long into the future. The couple’s children had forged successful careers outside the family business, but Sam dearly hoped his sons would take over the reins and continue the family legacy.

The Challenge

The Hatfields were asset rich; on paper they were worth upwards of $15 million, excluding their business. They owned their house in Melbourne’s leafy inner suburbs, had a holiday house on the Mornington Peninsula, and were debt-free. They had a significant amount of capital invested in a Self-Managed Superannuation Fund (SMSF). But their wealth was scattered and disjointed. They lacked an overarching structure to coordinate their various ad hoc investments and, more than anything, they needed a strategy for unlocking capital from the family business to shore up their retirement income.

Sam wanted to begin a conversation with his sons about taking over the family business, but he didn’t know where to start, nor did he understand the financial implications of an inter-family sale and how to effectively transition out of the business. The Hatfields had engaged a trusted accountant for many years who helped manage much of their financial affairs, but they needed broader advice beyond his expertise.

“How do start the conversation to transition a business to the next generation? How do you set up a program to assist the community, and involve the kids? What charities are suitable, what due-dilligence is needed? This was our challenge.”

The Goal

Sam and Kylie Hatfield’s ultimate goal was to preserve their wealth so they could maintain their lifestyle into retirement, enjoying all the things that make life worth living – dining out, overseas holidays, and entertainment with family and friends.

Their retirement security hinged on a successful transition out of the business that would unlock maximum capital with minimum tax liability. Sam also knew that he needed to diversify his investment portfolio and provide a support structure for Kylie, who had taken a backseat in their financial dealings.

When it came to supporting the rest of his family, Sam considered it imperative that he put structures in place to provide for the financial well-being of his children and grandchildren.

But he didn’t want to simply give them a cash handout; his contribution had to be structured in a measured and meaningful way that would fund their education and life opportunities without eroding their work ethic.

Like every family business owner, Sam worried that once he relinquished control of the business, his family’s hard-earned wealth was only ever one marriage break up away from being squandered.

He and Kylie had worked too hard to ever let that happen, and Sam knew he needed to seek legal advice about how to put provisions in place to protect the estate should one of his adult children divorce. Outside his family’s immediate interests, Sam also felt an intrinsic responsibility to his local community. He and Kylie were valued members of their local church and parish benefactors and also gave generous donations to various other charities. Sam didn’t want his community contribution to cease just because his work commitments had. It was important that he find a way to continue making a sustainable contribution to the causes about which he was most passionate.

As Stephan Independent Advisory, we see this situation as a very typical of a family business owner. Many business owners think of their business of being family nest egg for themselves, but when it comes to retirement there is more that they want to achieve with their finances. Like Sam and Kylie, many business owners leave their retirement and succession planning too late.

When you want to transition, it’s too late. Succession planning needs to come much earlier.

The Solution – a Personal CFO

Sam recognised that as a retiring family business owner he had complex wealth management needs. They were not the kind of needs that could be resolved in a one-off consultation with a financial planner; he needed a team-led by a personal CFO-to bring together all the threads of his financial, business, and family affairs.

“Sam engaged a wealth management advisor who devised an effective roadmap for his long-term financial prosperity.”

This wealth management advisor took a lead role in developing, mapping and planning a strategy for Sam and Kylie’s wealth management.

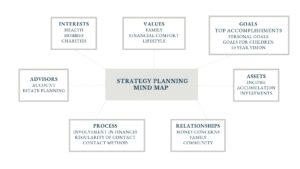

In an initial discovery meeting the advisor teased out all of the pertinent information about the Hatfields, their business, and the nuances of the family unit, including key stakeholders, assets, structures, life goals, values, and financial objectives.

Our Mind Map is where we start the strategy planning

Then, the advisor took a Lead role in engaging and coordinating with other expertise to deliver the plan.

The lead advisor coordinated the wealth management team, introducing each of the professionals to Sam and Kylie, organising meetings and clearly articulating their individual roles and responsibilities, as well as managing any areas of crossover.

Together the team of professionals came up with a holistic wealth management strategy that would be implemented over the course of one year and continually reviewed, in collaboration with the Hatfields. Each advisor took ownership of matters within their respective areas of expertise.

Sam and Kylie’s Wealth Management Team included:

- The Lead: a wealth advisor responsible for helping Sam and Kylie articulate and cost their retirement vision, and coordinating the wealth management team. In consultation with the accountant, the wealth advisor organised structures to ensure the couple’s wealth enhancement and protection into the future.

- A business consultant specialising in exit and succession strategies who helped Sam develop a plan and set a clear timeframe for transitioning out of the business.

- An accountant with best-practice financial experience in the manufacturing industry who provided a thorough valuation of the business. The accountant also analysed the business’s current financial structures, taking advantage of small business tax concessions that would enable the Hatfields to legitimately minimise their tax liability resulting from the sale.

- A commercial lending specialist who was engaged to undertake a comprehensive assessment of the financials, operations, and risks of the business. and prepare a proposal to put forward to their panel of financial institutions to assist in obtaining finance for Sam’s sons to acquire a portion of the business.

- An estate planning solicitor experienced in managing complex financial affairs where a family business is intertwined in the individual’s estate. The solicitor was responsible for ensuring Sam and Kylie’s assets were effectively distributed to their children and grandchildren in a manner that was flexible, tax-effective, and protected their assets, and provided Kylie with the necessary support mechanisms to effectively handle the estate should Sam predecease her.

An Example of a Coordinated Wealth Management Team

Without a coordinated wealth management team, driven by one lead advisor, there is a lack of cohesian, agenda and plans. This ends up with a scattered financial strategy.

The wealth management solution documented key recommendations, expected outcomes, deadlines, and tasks to be completed by nominated stakeholders.

During the implementation phase, selling and transitioning out of the business was identified as the key priority, and most resources and energy were funnelled into this task. At subsequent progress and accountability meetings the team assessed the initiatives completed so far and set their sights on the next implementation phase, which included developing a cash flow strategy and budgets post retirement, as well as reviewing and updating general insurances. Importantly, the Hatfields were actively involved every step of the way, and the process was methodical and calculated, drawing on the best minds in the business to minimise the chance of error and ensure that the solution best satisfied the identified goals and objectives.

We use a Strategy Map to track strategies and their progress

The outcome

The Hatfields successfully transitioned out of the business within a year, handing over the reins to their sons in a clear and methodical transition. They managed to minimise the tax they paid from the sale by taking advantage of small business concessions, and exited feeling confident that the business was in good hands and the family legacy protected.

Sam and Kylie are comfortable that they can live the retirement they’ve always dreamed of, with certainty around how much income they will be generating and its sustainability into the future. This is in part thanks to the diversification of their SMSF, and the reallocation of capital from property to other investment classes such as fixed interest and equities. They’re satisfied this will preserve their wealth in the long term and secure their retirement, regardless of any unexpected hiccups, including if something were to happen to Sam. Kylie has become more involved in progress meetings, has taken a greater role in understanding the family finances, and knows the support mechanisms available to her if her husband is no longer around. This is a great comfort to Sam.

The couple’s children and grandchildren are also taken care of, with the Hatfield’s intentions clearly articulated in estate planning documents. Furthermore, there are provisions in place to protect the family’s hard-earned wealth and ensure a structured and secure intergenerational transfer of assets going forward. As beneficiaries, the Hatfield children understand their responsibilities to the family business and how any family law issues will be resolved.

For the first time, Sam and Kylie feel the weight of the business lifted from their shoulders and know that their legacy will be protected and their financial future assured, no matter what happens.

{kind=link}

{kind=link}